"I can show you a text that changed a kid's life."

A college student may know basic financial literacy skills, such as how to open a banking account or balance a checkbook, but if they're drowning in $40,000 in school debt, does it really matter?

Debt is a ball-and-chain that 7 out of 10 students are blindly signing on for without knowing the full ramifications from years of school loans. Student loan borrowers graduate with an average of $37,172 in debt.

There are lots of options, resources, and ways to understand how to make the best financial decisions but something's broken. Why is student debt and the number of college dropouts still in the millions?

It's an information access problem; information is missing, confusing, inaccessible, and most of the time, it's just plain bad. What all students need, especially those from low-income backgrounds with a desire to go to college, is good information packaged uniquely for them in the right action-oriented medium.

One organization, Moneythink, has created an innovative way to help disadvantaged students enroll and graduate from college without crushing debt. A primary key to its process is text message-based coaching, which helps to increase college enrollment and reduce the number of college dropouts every year.

Students dropping out of college is a national problem

By 2020, 65 percent of jobs will require some level of postsecondary education. This is due in part to the ever-increasing role of technology in our economy.

But by next year alone, our country will have five million job openings requiring college degrees with no qualified applicants to fill them, according to the Georgetown Center on Education and the Workforce.

There are no qualified applicants because many students are dropping out of college, or not going at all.

Millions of students are dropping out of college

While overall educational attainment in the US continues to rise year over year, there are still 1.3 million college students dropping out.

The decision to drop out of college is complicated. It's not black and white and is far from being reduced to a single issue. However, the reasons given qualititatively by students, research, and federal statistics all point to one underlying cause—they couldn't afford it. Over 70% of dropouts cite high expenses and needing to work to make money as a main cause.

With sky-high college tuition rates and $1.6 trillion in debt crushing student bank accounts and already tight family savings, millions of students are dropping out of college with school debt and no diploma to show for it.

The Washington Post boiled the research down to one simple statement: that wealthy students graduate, and low-income students do not. Children from families earning more than $90,000 have a 1-in-2 chance of getting a bachelor's degree by 24. That falls to a 1 in 17 chance for families earning under $35,000, writes the Post.

6 specific reasons low-income students dropout of college

The research shows that money is the issue, but what does that mean exactly? If money is the common factor, then can simply more money solve the problem?

While it's true that financial pressure is the common thread, it does not account for the fact that every person's story is different. Universal solutions, applied as a blanket, do not effectively solve unique problems. Human lives are inspired to transform from the inside out not from the top down.

Aware of this complexity, Moneythink interviewed hundreds of college students across seven campuses to learn how financially insecure students (first-generation, working full-time, low-income, or students returning to school after a break) manage the financial challenges of pursuing higher education.

The study found six financial decisions in a young adult's life that cumulatively prevent a student from pursuing or finishing their college education.

- Housing. Tuition isn't the only major expense to attend some schools. Four-figure monthly housing bills need to be paid, too.

- Loans. If financial aid falls through, a student taking on $10,000-$20,000 of debt in a single semester can devastate their personal finances for decades to come, often leaving them with a lifetime's worth of loan repayment.

- Fragile scholarships. For low-income students who are lucky enough to receive scholarships, the loss of one can mean the loss of a degree.

- Short-term and long-term shocks. Car accidents. Health complications. Family duties. Any number of unfortunate incidents can happen any time, knocking a financially-insecure student out of college.

- Needing to work. The bills don't stop when one goes to college. In hard times, choosing between classes and income to pay bills is no longer a choice. Work comes first.

- Switching majors and colleges. For the students who need to stay in college for more than four years, often due to switching majors or transferring to another school, scholarships usually expire after four years, leaving dependent students scrambling for a solution.

These needs often run together, compounding the difficulty and stress weighing on a low-income young adult looking to enroll or trying to stay in college. For many, dropping out is the only way. In fact, one-third of college students drop out entirely, according to the National Student Clearinghouse Research Center. More than half of students enrolled in college take over six years to graduate. The Pell Institute found that it's worse for low-income students: Out of 100 low-income high school graduates, only 16 will complete a bachelor's degree in 6 years.

Sending text messages to low-income students works

A group of college students recognized this problem and started a club at the University of Chicago in 2008. The club members went to local high schools to teach students about personal finance. By the fall of 2011, the club—Moneythink—had grown organically from a student organization into a nonprofit volunteer movement on two dozen campuses across the country.

In 2016, Moneythink implemented an individualized approach that helps students navigate tough college financial decisions in a creative way.

The organization launched a college financial coaching program via a medium that students are already naturally using: texting.

"Through our data and student surveys, we're finding that action-oriented texting with a virtual coach (who was also most likely a first-gen or low-income student themselves) is the most effective and efficient way of reaching students," says Joshua Lachs, who succeeded Moneythink's Co ounder and long-time CEO in November, 2018.

A core principle that guides this design strategy of Moneythink is Don't give students more work. Texting is a pre-existing behavior that doesn't require the student to learn anything new.

"We empower and support students to solve difficult, often complex and life-altering problems through our texting and web-based coaching platform. We give students the tools, knowledge and know-how to make those decisions when they're making them, which is usually outside of the classroom, huddled with their family or feeling alone and stuck,"

Joshua Lachs, CEO of Moneythink

Moneythink is not your typical nonprofit

Moneythink operates like a nimble tech startup straight out of the Bay Area.

Where most nonprofits hire agencies to build software, Moneythink is one of the very few education nonprofits with an in-house product team. With a staff of 11, the organization leverages its own team of developers and designers to build its text message-based program, enabling the opportunity for massive scale with low overhead.

For example, one Moneythink coach can handle a caseload of 250 students.

"Our coaches are really unique in that they provide direct support to students and also serve as a learning lab for our product development. Because they work directly with students, our coaching team's proximity to students' challenges and strengths allows us to iterate and innovate in real time," said Josh Lachs.

The program currently serves 2,000 students in low-income high school districts in California and Illinois, like Solorio Public High School and Pittsburg High School in the Bay Area.

This year, Moneythink will expand its operations to Southern California; and by academic year 2020-2021, the organization plans to expand into other regions and states not only through high school partnerships, but additional youth-serving organizations and intermediaries, as well.

"Our five year vision is to help 320,000 students enroll in college with little to no debt—and help create an inclusive economy"

Joshua Lachs, CEO of Moneythink

How Moneythink works with schools

Currently, Moneythink is looking for high schools that have over 500 seniors, that have free or reduced lunch percentages of about 80% or higher, and have student-to-counselor ratios of over 400-500 to one.

The program is free to students. The Moneythink team comes in to the school one day to pitch to the entire senior class. "Our current model is opt-in for students and we use the highest degrees of privacy guidelines," said Lachs. "We're very transparent in how we can help them and that it's the students' decision whether or not they want to receive support from us."

The opt-in rates have been incredible. Last year, 90 percent of seniors signed up for Moneythink. This year, it's at 95 percent.

Moneythink helps students avoid debt

When a student goes through the onboarding period, they receive guides, tips, and advice, but perhaps most importantly, Moneythink starts to receive information from students, such as what their home life is like, which allows them to tailor the information they need to best help them.

From there, students receive a Moneythink coach, who is always there to answer questions, and also provide nudges and additional guides to ensure students are on top of different deadlines, and that they have quality, demystified information.

"Each student's experience is a little different," said Mike Jank, who recently stepped down as Moneythink's Development Director, where he served from 2017-2019. "We have students who are texting us every single day. We have students who are texting us once a month. We have students who are screenshotting questions in Spanish from their parents—we're a bilingual service, so we're able to support Latino families as well."

The coach helps remove barriers and motivate the student to accomplish important steps like filling out a FAFSA accurately and early, curate college options, compare financial aid award letters, and budget properly for college entry once they're on their way.

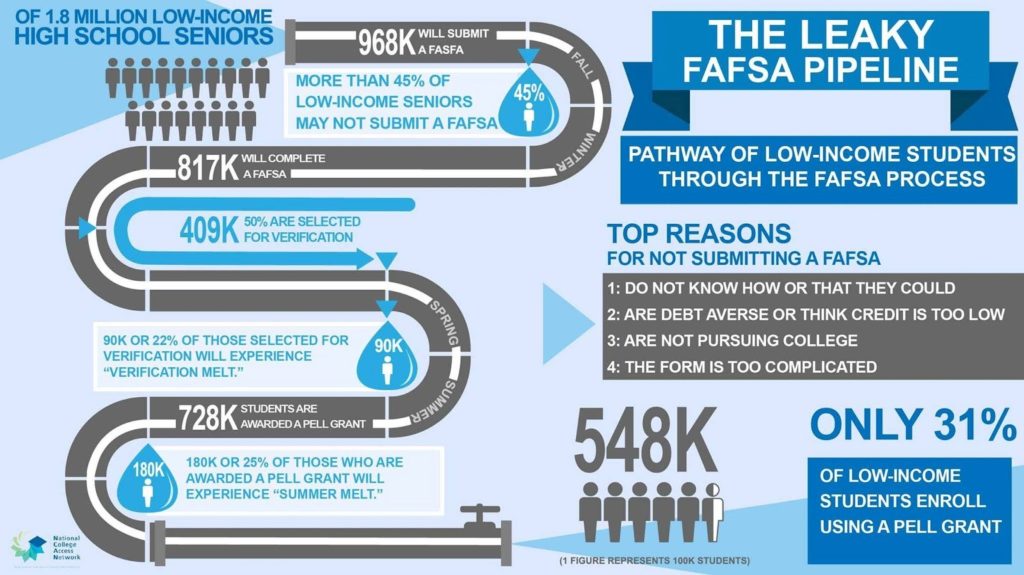

For example, financial aid is a critical component to student success, but last year only 31 percent of low-income high school students enrolled in college with a Pell Grant, a vital financial resource that need-based students can only qualify for if they fill out a FAFSA.

But, according to an alarming study by the National College Access Network, dubbed "The Leaky FAFSA Pipeline," the top reason students don't submit a FAFSA is because they "do not know how or that they could."

This is precisely the gap that Moneythink creatively fills via nudges and support through text messages. The results speak:

In Pittsburg High School where Moneythink is a critical partner, 83 percent of Moneythink students completed and submitted their FAFSA on time, compared to 58% for the rest of the eligible HS senior class. As for the entire state, Moneythink students rated almost 30% higher than similar students across all of California.

"College affordability is a big, nuanced problem that needs a bigger and simpler solution," said Joshua Lachs. "Leveraging our human-centered design approach, we see ourselves as an important contributor to build highly personalized, integrated, tech-enabled solutions at scale."

An avant-garde nonprofit, Moneythink is lighting the path forward for low-income students to receive college education and reach their full potential—without the burden of debt.

"We recurringly hear variations of the same message from our students: I don't think I would have ever applied to college and known how to pay for it if it wasn't for Moneythink," said Lachs.

"It's both humbling and inspiring to us as an organization," he said. "We're energized to keep going."

Joshua Lachs, CEO of Moneythink

***

Learn more about Stand Together's education efforts and explore ways you can partner with us.